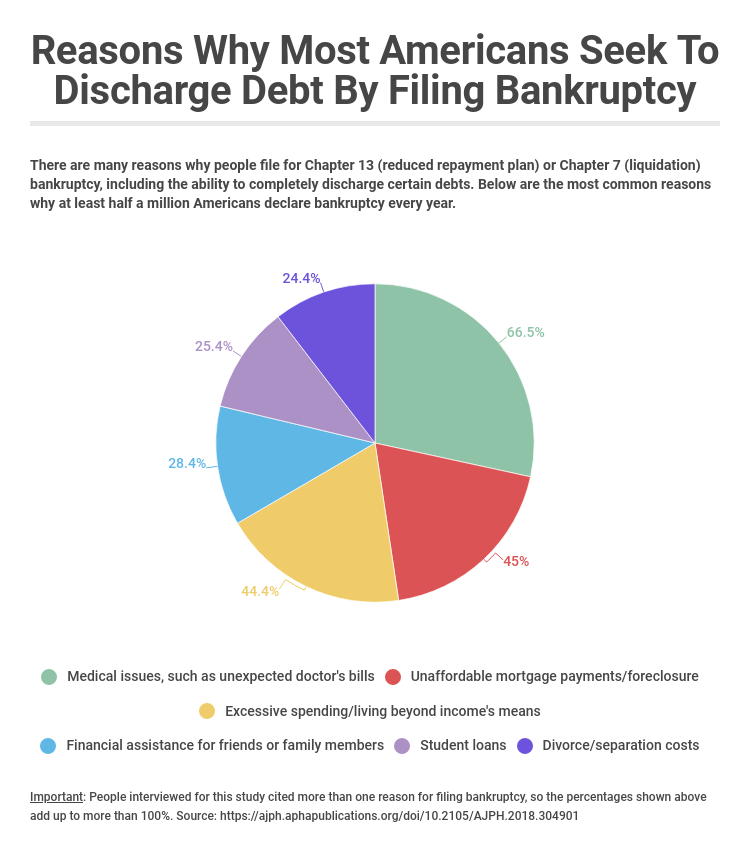

One of the many benefits of declaring bankruptcy is the ability to completely discharge certain debts. That’s right — once a court discharges them either through Chapter 7 or Chapter 13, you no longer owe those debts! Anywhere from 530,000 to 800,000 Americans filed for bankruptcy every year since 2010. See the most common reasons why below:

Which Debts Can You Discharge Completely Through Bankruptcy?

If bankruptcy court approves your petition, you can typically discharge the following debts completely:

- Credit card balances (about 99% of people who file discharge these debts)

- Medical bills

- Personal loans (i.e., check-cashing and payday loans)

- Past-due rent or other lease-related fees and fines

- Overpayments due to Social Security or the Department of Veterans Affairs

- Overdue utility bills

- Outstanding debt collection balances

- Checks written with insufficient funds (unless you wrote them fraudulently)

In some cases, you can also discharge older unpaid state and federal income taxes as well as property taxes. The laws may vary based on which state you live in, but generally, you can discharge those debts when:

- Past-due property taxes assessed more than one year prior to filing bankruptcy

- Unpaid state and federal income taxes owed at least three calendar years prior to declaring bankruptcy

Debts You Must Still Repay Even After Declaring Bankruptcy

Of course, there are some debts you cannot discharge no matter what type of bankruptcy case you file. Even if a judge approves your petition, there’s no way to avoid having to pay the following debts:

- Child support

- Alimony

- Unpaid/back income taxes less than three years old

- Federal student loans

- Loans taken out against your retirement plan (i.e., 401k, IRA)

- Mortgage or other property liens

- Car loans (the lender will simply repossess your vehicle)

- Debts from criminal or willful and reckless acts (DUI fines, speeding tickets, restitution payments owed for theft/embezzlement, etc.)

- Excessive credit card charges made within 90 days prior to declaring bankruptcy

That last one might give you pause. It’s because courts generally frown on people who go on “one last shopping spree” before declaring bankruptcy. If you decide to do this, prepare to have your bankruptcy petition dismissed in court. In addition, the court cannot discharge any debts you fail to list in your petition when you file. The good news is that depending on how you file, you can usually protect some assets, like your car and your home.

Lori Polemenakos is Director of Consumer Content and SEO strategist for LeadingResponse, a legal marketing company. An award-winning journalist, writer and editor based in Dallas, Texas, she's produced articles for major brands such as Match.com, Yahoo!, MSN, AOL, Xfinity, Mail.com, and edited several published books. Since 2016, she's published hundreds of articles about Social Security disability, workers' compensation, veterans' benefits, personal injury, mass tort, auto accident claims, bankruptcy, employment law and other related legal issues.